Sep

14

2015

Chicken Little once said that the sky is falling. Yet it still remains intact above us. So while the transition from magnetic stripe to EMV might seem like a shift of cataclysmic proportions, the sky is not falling. Your company will successfully transition from magnetic stripe to EMV (many already have), and next time you look outside your window, you’ll see the billowy clouds resting above, and not on the ground.

Chicken Little once said that the sky is falling. Yet it still remains intact above us. So while the transition from magnetic stripe to EMV might seem like a shift of cataclysmic proportions, the sky is not falling. Your company will successfully transition from magnetic stripe to EMV (many already have), and next time you look outside your window, you’ll see the billowy clouds resting above, and not on the ground.

Yet we also understand that with anything new comes fear. It’s normal. So we’ve put together a few facts to calm your nerves. We want you—the sagacious business owner that you are—to continue to make calm, smart decisions over the course of the transition.

Are you with us? Well, here goes:

In short, the sky is not falling, and EMV is not the end of the world. Instead, it seems to be the beginning to new possibilities for business owners. It might be an uncharted territory, but EMV will provide companies with the tools to chart their own course by allowing them to directly address fraud, a concern that leaves many involved feeling powerless. So next time you look at the sky, we at COCARD hope that you view it with possibility, and nothing less than that.

Read MoreRead More

True. Bats see just fine, and in spite of the idiom “blind as a bat”, bats really have no reason to serve as the benchmark for people with less than perfect eyesight.

Popular myths aside, fall is indeed upon us, which means that the start date of October 1st for the liability shift is near. Are you prepared?

To test your EMV preparedness, see if you can determine whether each statement is true or false.

There really is no proof that EMV is a safer way to protect data.

False, false, and false. Let’s look at two case studies. Since introducing EMV technology in 2004, the United Kingdom reported 62% less fraud in 2013. Canada has also reduced fraud losses to $29.5 million since transitioning to EMV technology. Fraud in Canada is down 79% from losses in 2009 ($142 million). With EMV technology responsible for the significant decrease in fraud in the UK and Canada, the technology aims to also decrease fraud in the United States as well, which currently accounts for nearly half of fraud worldwide.

All businesses—small and large—should be EMV-compliant.

True. No business is too small to adopt EMV technology. While it might be assumed that businesses with larger sales should adopt this technology, small businesses should also be sure to protect their sales as well. Leave it to a pesky fraudster to think ahead and target a small business because the merchant assumed that fraudsters only targeted larger companies. Prevent being caught off guard by being one step ahead of those who want to steal from you.

Adopting EMV technology is expensive.

For the business owner that thinks long term, false. The average cost of an EMV terminal is between $400 and $700. The average bill on a fraudulent card is $399. You do the math. While one fraudulent transaction probably won’t destroy you, starting October 1st, you, and not the associated bank, will be responsible for repaying losses resulting from fraud if your business is NOT EMV compliant. You will also be penalized for the fraud that could have been avoided by installing an EMV card terminal. When you add it all up, $400 to $700 is a small investment compared to the possible cost of not adopting the technology. What’s more, card processors such as COCARD often discount card readers. So call us today, and we will work within your budget.

In addition to business owners, employees should also be trained on how to properly use EMV technology.

True. While you are schooling yourself on the ABC’s of EMV, don’t leave your employees in the dark. Whether through workshops, a training program, or printed manuals, employees should understand how card terminals work for both themselves and customers who need assistance. COCARD can work with you to develop a training program that’s right for your company.

So how did you do? Did you get the right answers? Regardless, this information will be useful as your company prepares for the coming liability shift and transition to EMV. With foresight, you can protect your company from fraud and ensure, to the best of your ability, an environment that maximizes both security and profits. There’s nothing batty about it, EMV we mean.

Read MoreRead More

Watch out—the future has arrived. And they call it EMV. As the target date for businesses to accept EMV payment cards draws near, make sure your business is ready to transition seamlessly from magnetic stripe cards to EMV. October 1st is upon us. Are you ready?

Watch out—the future has arrived. And they call it EMV. As the target date for businesses to accept EMV payment cards draws near, make sure your business is ready to transition seamlessly from magnetic stripe cards to EMV. October 1st is upon us. Are you ready?

This list of FAQs will help you answer lingering questions and stay abreast of new developments with EMV technology.

What does EMV stand for?

It is an acronym for its developers Europay, Mastercard and Visa.

What’s the main difference between the cards we use now and EMV cards?

Magnetic stripe cards are the cards currently used in the United States and have a magnetic strip on the back. These cards are swiped through a card reader and contain static financial information that can be easily duplicated by card readers. EMV cards, on the other hand, contain a microchip that produces a new code with each transaction, preventing fraudsters from gaining access to sensitive data on the card. EMV cards are therefore more secure than magnetic stripe cards, and are responsible for a worldwide decrease in fraud.

How will switching to EMV directly benefit my business?

Great question. EMV will benefit your business threefold. First, your risk of chargebacks based on fraudulent transactions is greatly reduced. Whereas banks bore the brunt of the financial weight for fraud in the past, companies that have not adopted EMV technology will now be held accountable starting October 1st, when the liability shift starts. Adopting EMV technology will protect your business from costs associated with fraud. Second, as technology evolves faster than you can say Darwin, EMV is simply the beginning. Most of the hardware that accepts EMV will also allow your business to accept payment innovations such as mobile apps (i.e. mobile couponing and loyalty programs) and contactless payments. Third, you will be able to accept payment from visitors from other countries. Much of the world has already adopted this technology and no longer uses magnetic stripe cards. So prepare your business to increase profits by switching to a payment technology that more people can use.

I’ve been hearing the term “liability shift” a lot lately. What exactly is it?

It is when liability for card fraud switches from banking institutions to merchants. On October 1, 2015, businesses that aren’t updated to accept EMV cards will be held responsible for card swiped transactions on EMV capable cards that are found to be fraudulent. And penalties can be costly, particularly for small businesses. However, if your business is EMV-compatible, you will not be held accountable for fraudulent transactions.

As a small business owner, every penny counts. How much will it cost me to install an EMV-capable terminal?

EMV card readers cost between $400 and $700 but are often discounted through payment processors such as COCARD. Speak with us today—your EMV solution might even be free.

One thing to remember is that as the United States fully transitions to using EMV technology, cards will include both the microchip and magnetic strip. The process is expected to take anywhere between three and five years.

COCARD aims to develop our reputation as experts on EMV. We will continue to keep you posted on new developments and new ways of looking at this groundbreaking technology.

Read MoreRead More

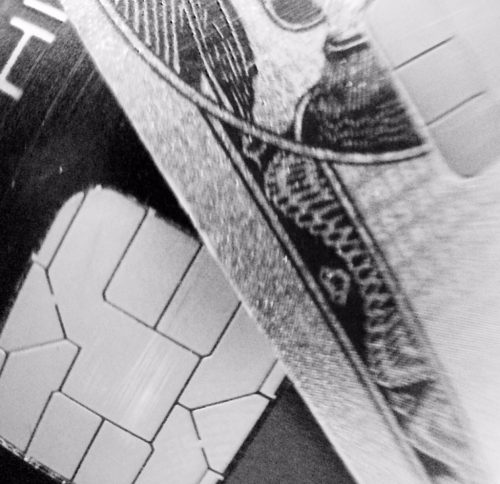

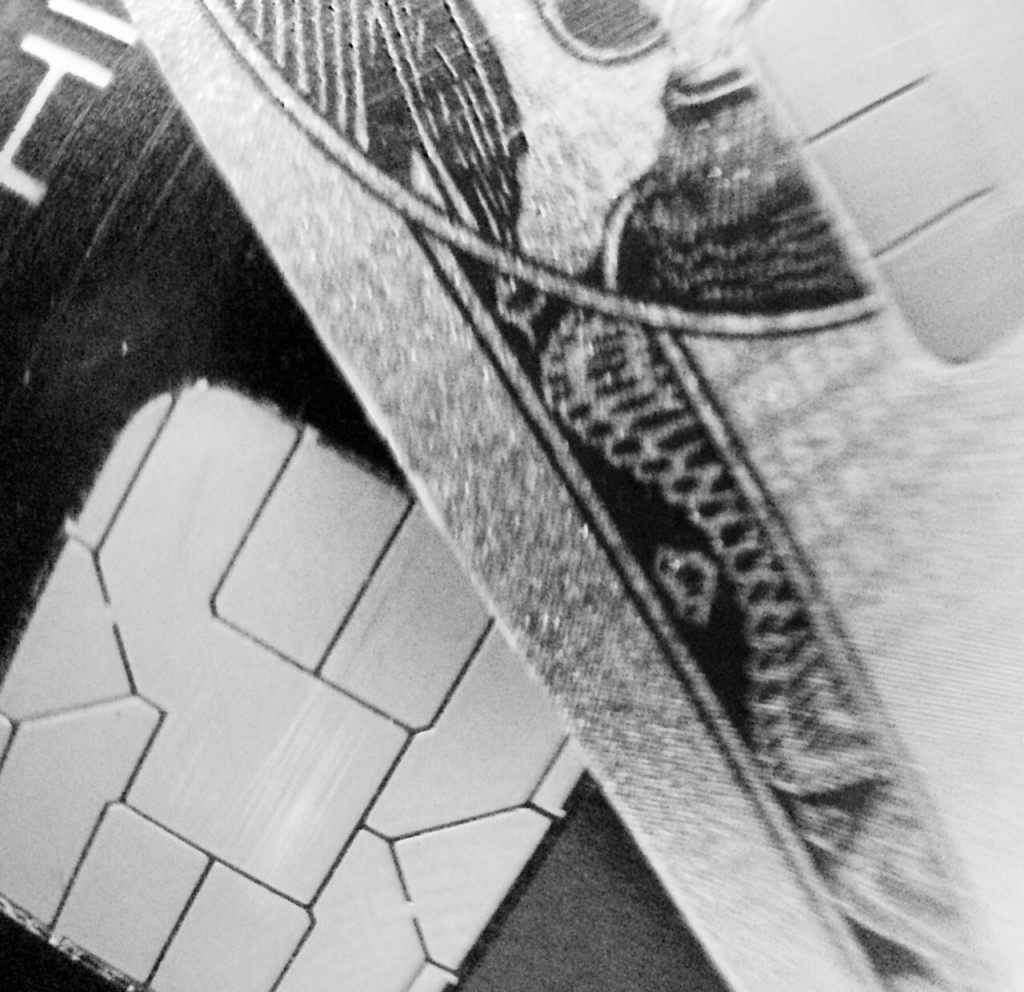

Maybe you’ve already gotten a glimpse; a customer pulls a credit card out of his or her wallet, and as they swipe, you see a chip that’s embedded in the card. Don’t freak out. You don’t have to work at Google to get it. You just have to understand a few simple points about this new chip.

Maybe you’ve already gotten a glimpse; a customer pulls a credit card out of his or her wallet, and as they swipe, you see a chip that’s embedded in the card. Don’t freak out. You don’t have to work at Google to get it. You just have to understand a few simple points about this new chip.

Let’s demystify the mystery, decode the data, and simplify the complexity of EMV.

• Update, update, update. EMV technology is new to the US, and the truth is that not all POS machines are already EMV-capable. What this means is that you should check both your hardware and software to see which components (whether some or all) should be updated, which brings us to our next point.

• Stay connected with all parties involved. No EMV machine is an island unto itself. Your POS system requires cooperation with your bank, processor, and other individuals or companies connected to your POS system. Find out what they have to say about EMV to stay current with any updates regarding the technology. It will allow for a more seamless transition.

• Think smart. Plan ahead, and stay one step ahead of the game. Once you’ve got the ball rolling on updating your POS system, consider other ways in which your system can stay smart. This includes considering a cloud-based POS or tablet solution like Revonu POS by COCARD.

• Consider COCARD. If you are considering a POS provider, we have a number of options available for POS systems and can help you decide if a new system is right for you.

• Carry an umbrella. You should always plan for a rainy day. Although it’s unlikely, there is always the slight possibility that your POS will break down. It isn’t fair, we know; but stuff happens. You should make a back-up plan to prepare for the off chance of the unexpected. Did you know that the Revonu package by COCARD includes a FREE EMV terminal?

• Teach your employees to fish. We promise, this is the last metaphor. Here at COCARD, we believe that employees should be trained in the ways of EMV. That means that they should understand the technology and know how to use it. After all, having truly knowledgeable employees makes the company look good.

So that’s it, six key points to remember about EMV. As you continue to learn more about this new technology, use this as a basic guide during your company’s transition to EMV.

The EMV experts at COCARD are available to answer any questions you may have!

800-317-1819 or support@cocard.info

The complete POS solution for YOUR business!

The complete POS solution for YOUR business!Let us tell you about our simple and cost-effective combined point of sale solution. It’s Revonu; helping main street generate more revenue.

For more information about Revonu call – 1-800-317-1819 option #2, visit us on the web at: http://cocard.info/products/revonu/ or email revonu@cocard.info

Read MoreRead More

Integrated hardware,cloud software & payment solutions.

Integrated hardware,cloud software & payment solutions.Spend more time on the front-end of your business with our simple and cost-effective combined point of sale solution. By pairing state-of-the-art hardware with reliable cloud software and PCI compliant merchant processing, we’ve eliminated the hassle of dealing with multiple providers while allowing access to your business 24/7.

For more information about Revonu call 1-800-317-1819, email revonu@cocard.info or visit Revonu at http://cocard.info/products/revonu/

Read MoreRead More

Did you know that nearly half of all credit card fraud worldwide occurs in the United States? Considering that only 24% of credit card sales are made in the US, this number is surprisingly high. To combat fraud, the United States is currently transitioning to credit cards that use EMV technology, which will increase security and reduce fraud for all credit card transactions. The technology is slated to revolutionize the way you do business by allowing merchants to transition to a safer standard of payment processing.

What exactly is EMV, you might ask? Taken from the name of its original developers Europay, Mastercard, and Visa, the technology includes a microchip embedded into a credit card that produces a one-time code each time it is used. A customer will still verify the transaction with either a signature, pin number or both. Small transactions, however, may not require either.

Because a new code is produced with each transaction, the cardholder’s personal information remains secure. Here’s why.

If a hacker does in fact steal information from a specific point of sale and replicates the card, the new card will be denied since the information on the original card changes with each new transaction. The stolen information is invalid—it was only valid with the cardholder at the time of purchase.

Cards with magnetic stripes, on the other hand, can be duplicated easily with a card-reading device. This device skims card information allowing criminals to create counterfeit cards.

Eighty countries have already adopted EMV chip technology. The United States will be one of the last countries to adopt this technology. By the end of 2015, the United States will have issued 70% of credit cards and 40% of debit cards as EMV cards.

What this means for merchants is that your business will need to soon become EMV-compliant, if it isn’t already.

The target date to acquire this technology will be October 1st of this year, at which point the Liability Shift starts. Merchants who are EMV-compliant will not be liable for losses due to card fraud; but if a merchant is not EMV-compliant, he or she will bear the cost of fraudulent activity. Prior to, banks were responsible for bearing the costs associated with card fraud.

To ease the transition, which is estimated to take three to five years, credit and debit cards issued in the United States will include both microchips and magnetic stripes.

The future of payment processing is upon us. Prepare your business to succeed by working with COCARD to transition to EMV technology today.

Read MoreRead More

You are probably hearing a lot about EMV in the news and maybe even receiving a few scary calls from merchant service providers who imply that EMV has something to do with PCI Compliance. For the record EMV has NOTHING to do with PCI Compliance and no matter what software you are running on your POS COCARD can manage your EMV. Relax, COCARD is ready for EMV and we are here to help YOU be ready too.

You are probably hearing a lot about EMV in the news and maybe even receiving a few scary calls from merchant service providers who imply that EMV has something to do with PCI Compliance. For the record EMV has NOTHING to do with PCI Compliance and no matter what software you are running on your POS COCARD can manage your EMV. Relax, COCARD is ready for EMV and we are here to help YOU be ready too.

A little background: EMV stands for Europay, MasterCard and Visa; it is the global standard for cards equipped with computer chips and the technology used to authenticate chip-card transactions. Have you heard about all the data breaches in the last few years? EMV is the card association’s answer to these breaches, the technology has been used in Europe for more than 10 years and they have seen a drastic reduction in credit card fraud.

What happens?

In the beginning your exposure will be minimal because the only liability for fraud will be with cards that have chips implanted. However, as time goes on, and if EMV becomes the new standard, your exposure will increase. If a chip card is used at a business that has not changed its system to accept chip technology and this chip card is fraudulent then the counterfeit card can be successfully used and cost of this fraud will fall back on the merchant.

What does this new technology mean to your business?

The switch to EMV means adding a new in-store technology to your current processing system or not. Chances are you may already be EMV ready but in either case don’t worry, COCARD is here to help! Most importantly the EMV technology means greater protection against fraud in your business.

For ongoing updates and the most current information about EMV, PCI, card association updates and fraud alerts like us on Facebook and follow us on Twitter.

Read MoreRead More

Big news for the service industry: 2014 has brought a huge surge in the number of service-related companies. According to a recent article in Bloomberg, service industries—like restaurants and retailers—grew in July at the fastest rate since December 2005! Additionally, the Institute for Supply Management’s (ISM) non-manufacturing index increased to 58.7 (readings greater than 50 indicate expansion). The U.K. is experiencing similar trends in its service industry as well, which means your potential customers are ready and willing to spend. Terry Sheehan, an economist at Stone & McCarthy Research Associates is cited in the article as saying, “We’re seeing numbers that we haven’t seen since well before the financial crisis and recession, and they seem to be more sustained.”

Coinciding with this jump are an increase in new orders among service providers (they too are experiencing the highest ISM measure since August 2005) and an uptick in production (manufacturers have the highest ISM level since April 2011). Negative side-effects include an increased unemployment rate from 6.1 percent to 6.2 percent (given the influx of new job seekers into the labor market), a decline in the stock market (investors jumping on the anticipated uptick too soon) and an increase in competition for businesses in the service industry.

Worried about the influx of new competitors? Stay ahead of the curve by employing these business practices.

Read MoreRead More