Mar

08

2018

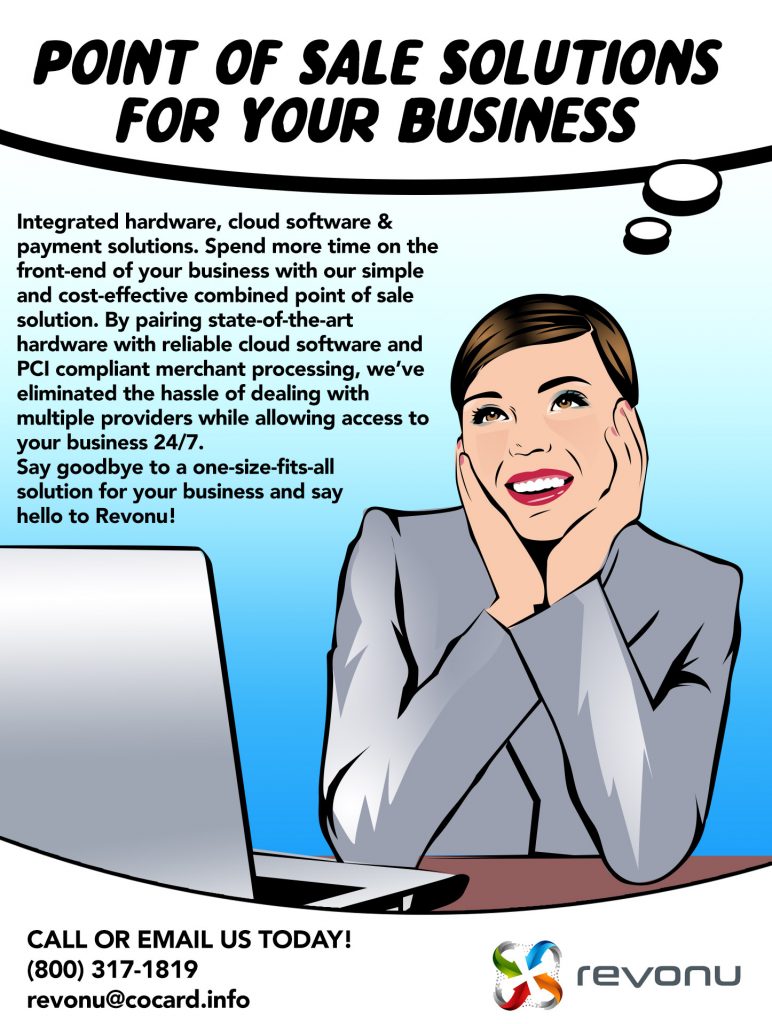

As a business owner, nothing is more rewarding than seeing your company grow and thrive. After all, you are the one putting it all on the line, calling the shots and making important decisions that will lead to your future success. Because business trends change there are times, you may have an abundance of income; others, you may be low on capital. If you find yourself short of cash and need to purchase key equipment like a new point of sale system, make necessary repairs or have a lucrative opportunity, you may want to explore funding options. One option – a merchant cash advance – offers rapid access to cash with minimal qualifications and formalities. Interested, contact our office today and let’s talk about what you need to keep your business growing in 2018!

As a business owner, nothing is more rewarding than seeing your company grow and thrive. After all, you are the one putting it all on the line, calling the shots and making important decisions that will lead to your future success. Because business trends change there are times, you may have an abundance of income; others, you may be low on capital. If you find yourself short of cash and need to purchase key equipment like a new point of sale system, make necessary repairs or have a lucrative opportunity, you may want to explore funding options. One option – a merchant cash advance – offers rapid access to cash with minimal qualifications and formalities. Interested, contact our office today and let’s talk about what you need to keep your business growing in 2018!

1-800-317-1819 Ext 4360 and talk to one of our cash advance specialist

Read MoreRead More

It’s Wednesday, “HumpDay”. Ever wonder where the term “HumpDay came from? Wonder no more!! Check out this link and Hey Happy HumpDay!

It’s Wednesday, “HumpDay”. Ever wonder where the term “HumpDay came from? Wonder no more!! Check out this link and Hey Happy HumpDay!http://frontporchdenver.com/where-did-the-term-hump-day-come-from/

Read MoreRead More

It’s Friday – Friday – Friday!! TGIF !! Check out these tips for a great Friday, have a wonderful weekend!

It’s Friday – Friday – Friday!! TGIF !! Check out these tips for a great Friday, have a wonderful weekend!

https://www.livehappy.com/self/10-tips-happy-friday

Read MoreRead More

As we find ourselves in the second month of 2018, we at COCARD would like to do a quick check in for any New Year’s resolutions you may have made this year, or things that you’d like to improve on for the upcoming year. From money management skills to planning, how have you been doing with these things since January 1st?

How do you manage the money that goes in and out of your business? Money is the lifeline that keeps your doors open, and your business running. Without it, you and your business will have a difficult time existing. Did you know that 82% of startups and small businesses fail because of a lack of cash flow, according to a study from U.S. Bank, a financial services company? So take stock of where your money is coming from, and if needed, take stock of tip #2, reviewing your rates.

It is one thing to charge one rate as you start, but another thing to keep the same rate as you’ve gained more experience and can prove the value that you bring to another business or company. So look at rates in your industry, and make sure that you are charging a rate that fits your experience and worth. Anything less would be criminal, and would hinder your ability to bring in the right amount of money for your business and livelihood. So do your research, and even write down the value that you’ve provided to customers. Then set new rates.

As a professional in your field, you should continue to learn. Learning doesn’t stop after you make a certain amount of money. It also doesn’t stop after you’ve reached a certain professional marker. To stay current and at the top of your game, you should read books, take courses, and attend events that will help you to keep developing your skills. In this way, your business will continue to evolve for the better, and can continue to compete in the marketplace.

If you come up against obstacles or questions, you should focus on the things that work for you. If something isn’t working, toss it aside, and continue moving forward. This method allows you to make room for something else in the future, something potentially much better than what you had before.

As the year progresses, it is important for us as business owners to take stock of the roads we are taking and how we will get there, to our destinations. For all of us, “there” often means profitability along with a strong bond with our customers.

What else have you taken stock of as a business owner since this year has started?

Read MoreRead More