POS and Your Salon

The Beauty industry is growing, fast. If you have chosen to open a Salon, you may have picked the best time to do it. You’ve already done the hard part. Make the business plan, found the space, curated an environment for your clientele that best reflects you and the business you care so much about. The next step should be easy, provide excellent customer service that will keep your door swinging time and time again.

The Beauty industry is growing, fast. If you have chosen to open a Salon, you may have picked the best time to do it. You’ve already done the hard part. Make the business plan, found the space, curated an environment for your clientele that best reflects you and the business you care so much about. The next step should be easy, provide excellent customer service that will keep your door swinging time and time again.

In business, timing is everything. Now might be the perfect time to consider a Point of Sale system instead of the usual electronic cash register. It is true that when starting a business sometimes the easiest option that poses the least financial burden seems like the best option. However, if longevity and efficiency is what you’re looking for. A POS system might just be for you. So, let’s look at the advantages a POS system could bring to your Salon so you can focus on the beauty side of things.

- With the recent boom in popularity of using digital payment options It is important to fit your Salon with the technology required to stay ahead of the curve. With over 50% of US merchants now accepting Apple pay, you can join the wave of Salon owners who choose to keep their businesses on the forefront of the digital age.

- Easy to use systems make for a faster experience for the customer and are easier to use for your employees. Training to use such a system is simple and free of stress, making your Salon more productive and leaving the customer with a more positive experience overall.

- A POS system will allow you to spend less time scheduling and managing your employees and more time with the client in your chair. Modern POS terminals include clock in/clock out functionality. Perfect for the busy Salon you’ll be running!

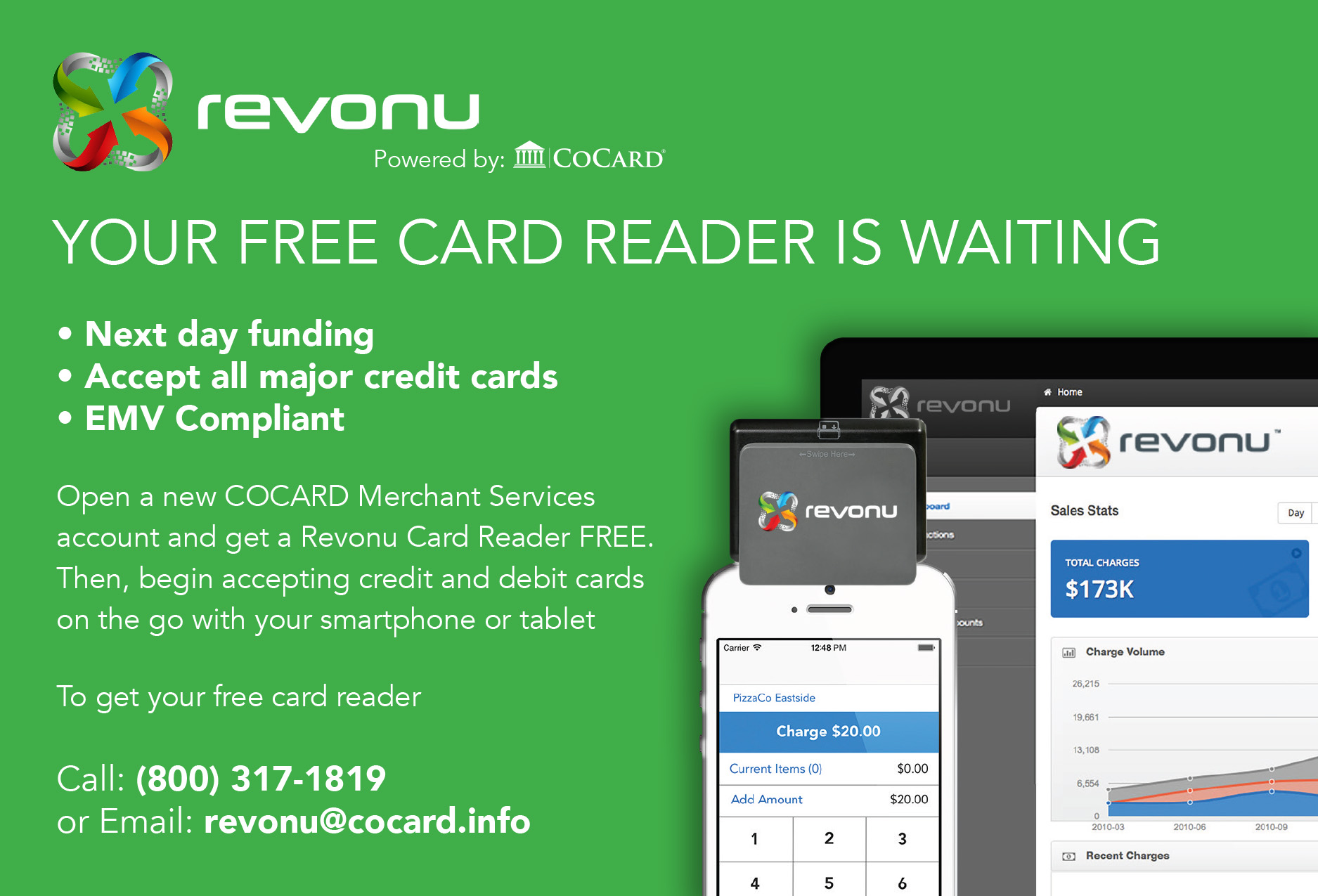

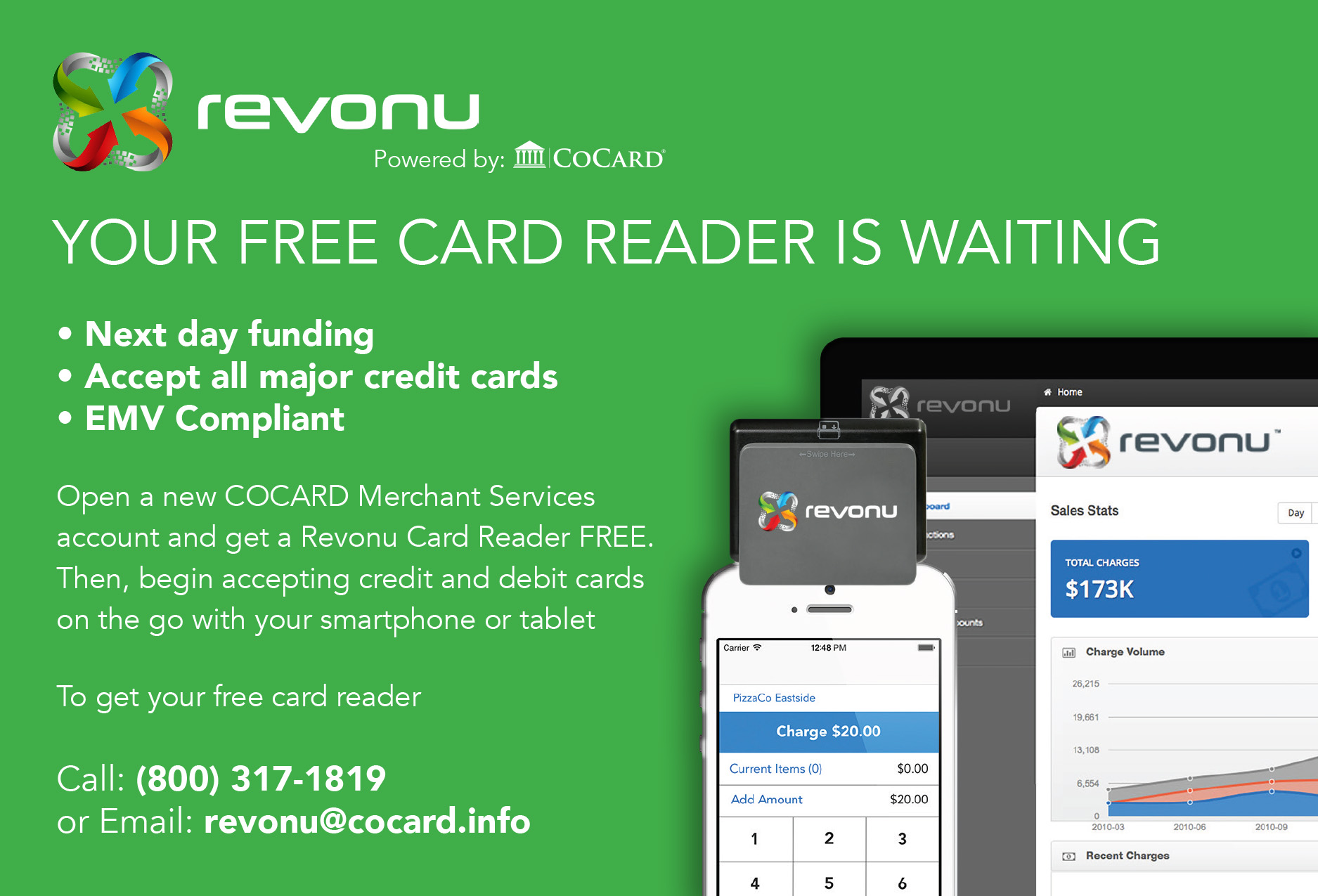

These are just a few of the many ways you can make a POS system work for you. For more information on the systems available from CoCard, head to our main website at www.cocard.info.

Read MoreRead More